Why That “KSh 5M Deal” Might Actually Cost You Much More

When it comes to real estate, many buyers focus only on the listing price—but the hidden closing costs of buying property in Kenya are what truly determine whether a deal is affordable or financially overwhelming. From stamp duty and legal fees to utility connections and post-purchase expenses, these additional costs can add 5% to 15% on top of the property price. Understanding them early is the difference between a smooth purchase and a stressful one

What Are Closing Costs—Really?

Closing costs are everything you pay after you’ve agreed on the property price.

They are not optional. They are not “nice to have.”

They are the difference between owning a property on paper and actually becoming the legal owner.

These costs typically include:

- Government taxes

- Legal fees

- Bank and valuation charges

- Registration and documentation

Individually, they may seem manageable. But combined? They reshape your entire budget.

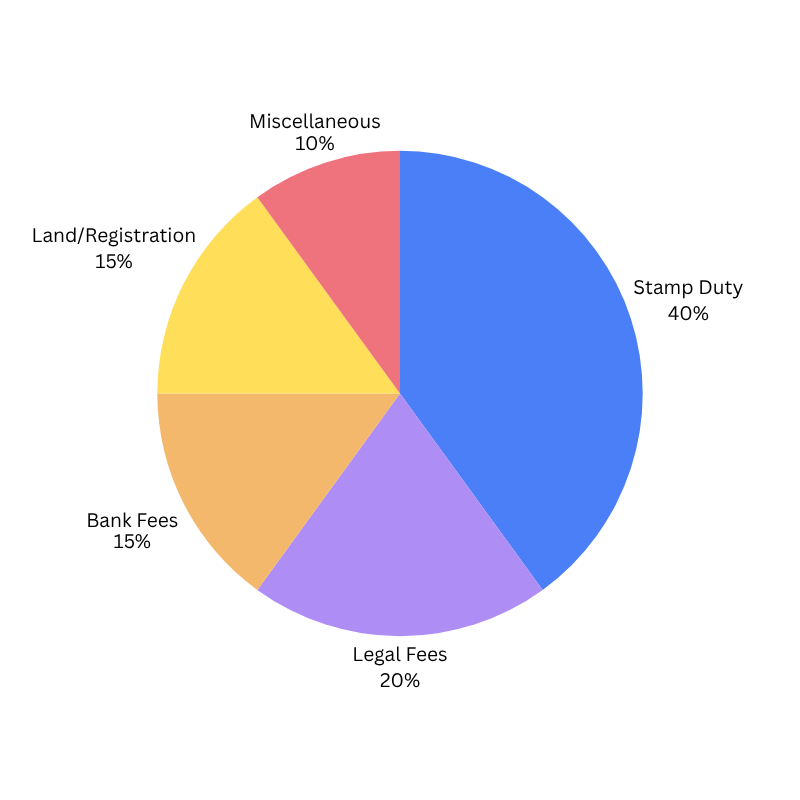

1. Stamp Duty: The Biggest Hidden Closing Cost in Kenya

If there is one cost that consistently surprises buyers, it’s stamp duty.

This is a government tax paid to transfer property ownership—and in urban areas like Nairobi, it stands at 4% of the property value (2% in rural areas).

Let us make it real:

You agree to buy a property at KSh 5 million in Nairobi.

That means you’ll pay KSh 200,000 in stamp duty alone.

And here is where it gets even more interesting—

Stamp duty is based on government valuation, not your negotiated price.

So even if you negotiate well, the tax may still reflect a higher assessed value.

This is often the first point where buyers pause and ask: “Wait… I didn’t budget for this.”

2. Legal Fees: The Cost of Sleeping Peacefully at Night

It’s tempting to see legal fees as an area to “save money.” After all, you’ve already found the property—what else is left?

A lot.

A qualified property lawyer does more than paperwork. They:

- Confirm the seller actually owns the property

- Check for disputes, loans, or encumbrances

- Handle the transfer process correctly

Legal fees in Kenya typically range from 1% to 2% of the property value.

So for an KSh 8 million property, you’re looking at roughly KSh 80,000 to KSh 160,000.

Skipping this step isn’t saving money—it’s risking everything you’ve worked for.

We’ve seen cases where buyers “trusted the process” and ended up entangled in disputes that cost far more than legal fees ever would.

3. Bank and Valuation Costs: When Financing Comes In

If you’re financing your purchase through a bank, there’s another layer of cost to consider.

Before approving your loan, the bank will:

- Conduct a valuation of the property, the valuation is done by a vauer register by the Valuers Registration Board

- Charge loan processing fees

Typical costs include:

- Valuation fees: 0.25% to 0.5%

- Loan fees: 1% to 1.5%

For example, a KSh 6 million loan could easily come with KSh 60,000 or more in additional charges.

It’s not just about qualifying for the loan—it’s about affording everything that comes with it.

4. Land and Title Costs: Small Numbers, Big Importance

These are the quiet costs that rarely get attention—but they are essential.

They include:

- Title registration

- Land searches

- Clearance certificates

You might spend up to KSh 30,000 or more here.

Individually, they feel minor. But without them, your ownership is incomplete. This is the administrative backbone of your investment.

5. Buying Land? There’s More Beneath the Surface

Land purchases come with their own realities.

What looks like a clear, open plot may still require the following:

- A surveyor to confirm boundaries

- Beacon verification

- Fencing and basic security

A proper survey can cost anywhere from KSh 20,000 to KSh 100,000. Costs related to fencing can also quickly climb into six figures depending on size and materials.

The hard truth is that visible boundaries are not legal boundaries. We always advise buyers to never rely on what you see. Ensure that you verify what is documented.

6. The “Last Mile” Costs: Where Budgets Break

This is where many buyers get caught off guard.

You’ve bought the property. The paperwork is done. Everything feels complete. Then you realize that water is “available”—but not connected. Electricity is nearby—but needs poles and installation. Internet is also another setup entirely.

These “last mile” costs can easily exceed KSh 100,000, depending on location. They come at a time when most buyers already feel financially stretched.

7. Ownership Doesn’t End at the Title Deed

There is a common assumption that once you’ve paid for the property, you’re done, but in reality, you are just getting started.

Post-purchase costs often include:

- Moving expenses

- Furniture and appliances

- Repairs and repainting

- Service charges (for apartments)

Furnishing a modest 2-bedroom unit can range from KSh 200,000 to KSh 600,000. This is the difference between owning a house—and actually living in it comfortably asa home.

Who Pays What? Never Assume

One of the most common sources of confusion in property transactions is responsibility.

In most cases:

- The buyer pays: stamp duty, legal fees, valuation, and registration

- The seller pays: land rates and Capital Gains Tax (CGT)

But here is the key: Always confirm this in writing, every agreement can be structured differently.

A Real Nairobi Example

Let us bring this closer home. You’re buying a KSh 2 million plot near Nairobi.

Here’s what your additional costs might look like:

- Stamp Duty → KSh 80,000

- Legal Fees → ~KSh 35,000

- Survey → KSh 20,000

- Miscellaneous → KSh 5,000

Total extra cost: ~KSh 140,000

That is roughly 7% above the purchase price—and that is on a relatively modest deal.

The Smart Buyer’s Approach

The difference between a stressful purchase and a smooth one is rarely luck—it is preparation.

Experienced buyers always do the following:

- Budget an extra 7%–10% minimum

- Ask for a full cost breakdown early

- Work with professionals (lawyers, valuers, surveyors)

- Avoid undocumented or rushed transactions

Because in real estate, surprises are expensive.

The Bottom Line

The hidden closing costs of buying property in Kenya are not optional—they are part of the investment. The earlier you understand them, the better you position yourself to make confident, informed decisions.

At Bekhan Homes, we don’t just help you find property. We help you understand what it truly takes to own it—so you can move forward with clarity, confidence, and control. Talk to an expert before you buy that property.